Load the data set into R environment. This data set is collect by Walmart for researching variables that might influence the CPI score (Consumer price index).

[DOWNLOAD HERE]

data =read.csv('../data/walmart.csv')head(data)

A data.frame: 6 × 9

Store

year

month

day

Temperature

Fuel_Price

CPI

Unemployment

IsHoliday

<int>

<int>

<int>

<int>

<dbl>

<dbl>

<dbl>

<dbl>

<lgl>

1

1

2010

2

5

42.31

2.572

211.0964

8.106

FALSE

2

1

2010

2

12

38.51

2.548

211.2422

8.106

TRUE

3

1

2010

2

19

39.93

2.514

211.2891

8.106

FALSE

4

1

2010

2

26

46.63

2.561

211.3196

8.106

FALSE

5

1

2010

3

5

46.50

2.625

211.3501

8.106

FALSE

6

1

2010

3

12

57.79

2.667

211.3806

8.106

FALSE

Simple plots

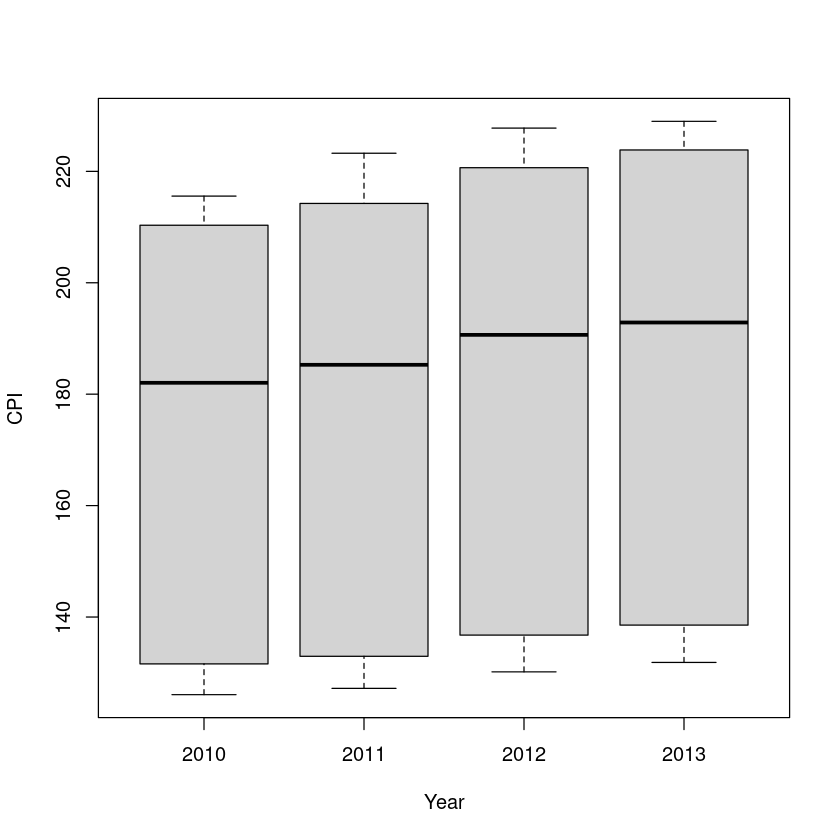

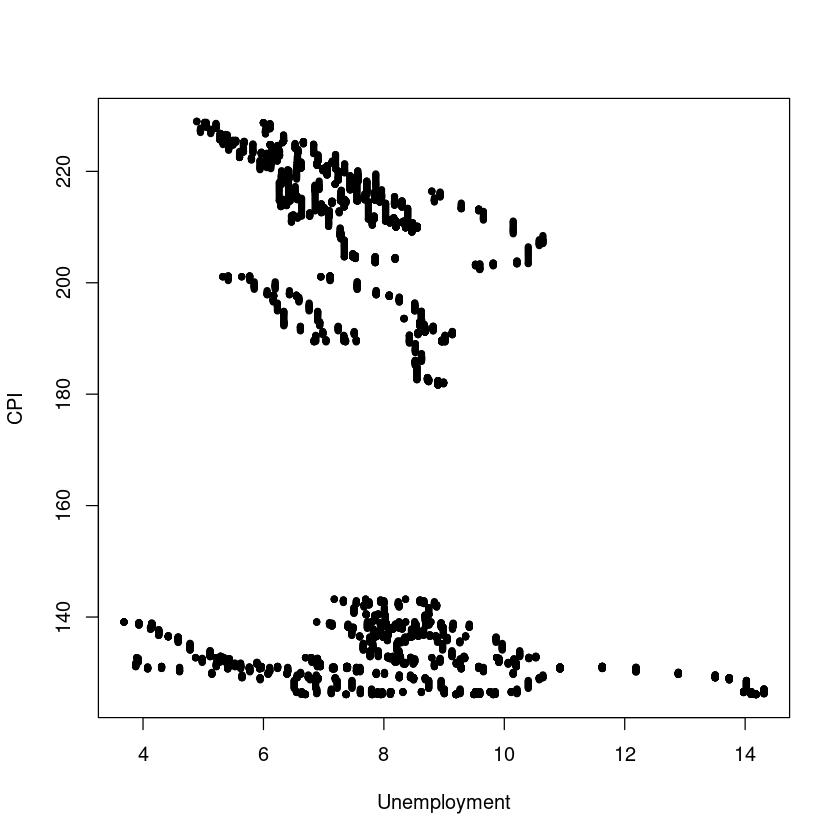

Making some simple plots is a smart way of knowing our data set in the first stage. Try to make all following plots. What conclusion can you make by observing?

A side-by-side boxplot

plot(x =factor(data$year), y = data$CPI, xlab ="Year", ylab ="CPI")

Welch Two Sample t-test

data: cpi2010 and cpi2012

t = -6.4642, df = 4497, p-value = 1.127e-10

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-9.924313 -5.305366

sample estimates:

mean of x mean of y

168.1018 175.7166

Test if the fuel price in 2010 and 2012 are the same. Then, assume that the population variance is the same.

Two Sample t-test

data: fuel2010 and fuel2012

t = -119.71, df = 4498, p-value < 2.2e-16

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-0.8622102 -0.8344239

sample estimates:

mean of x mean of y

2.823767 3.672084

Correlation coefficient

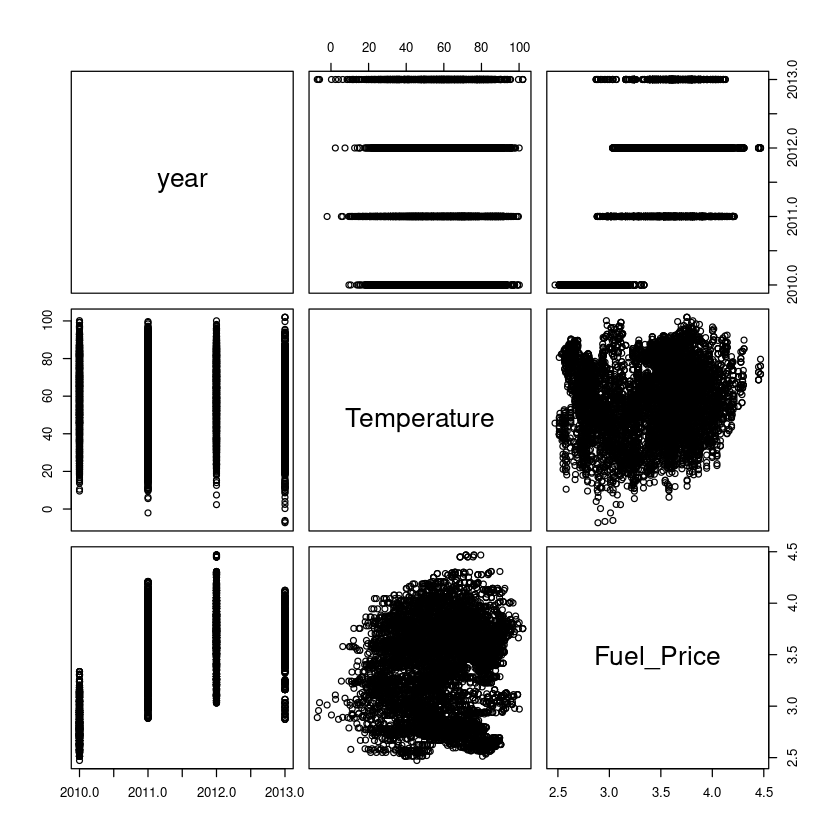

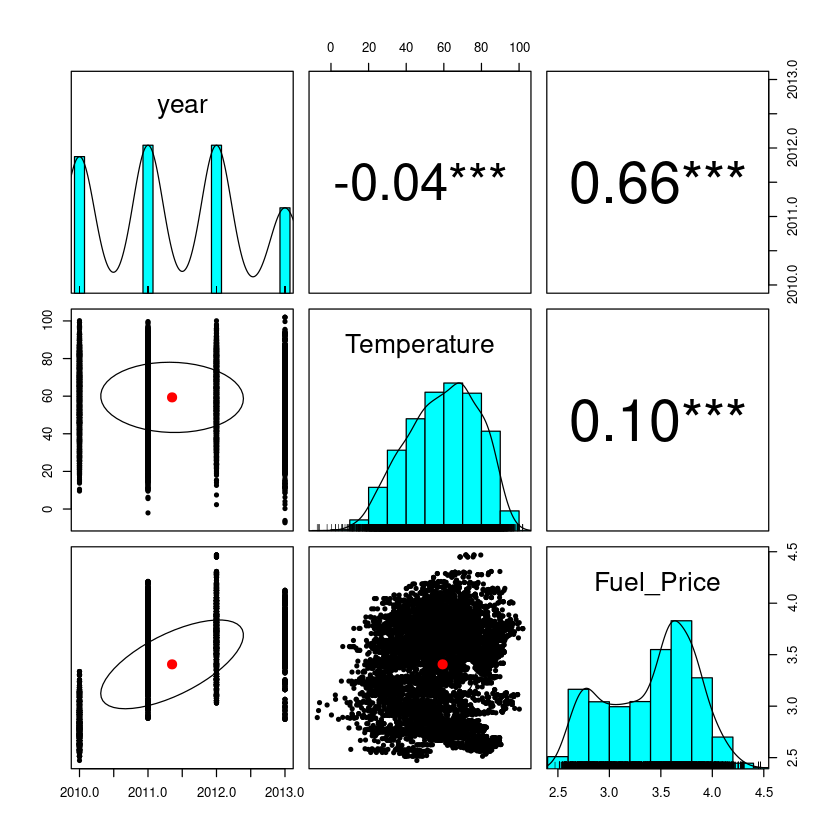

Calculate the pairwise correlation between year, temperature, and fuel price. Present it in both the plot (scatter plot) and correlation matrix.

cor(data[, c(2, 5, 6)])

A matrix: 3 × 3 of type dbl

year

Temperature

Fuel_Price

year

1.00000000

-0.03837331

0.6577771

Temperature

-0.03837331

1.00000000

0.1013542

Fuel_Price

0.65777712

0.10135422

1.0000000

plot(data[, c(2, 5, 6)])

Advanced

Try this section after you finish all previous sections

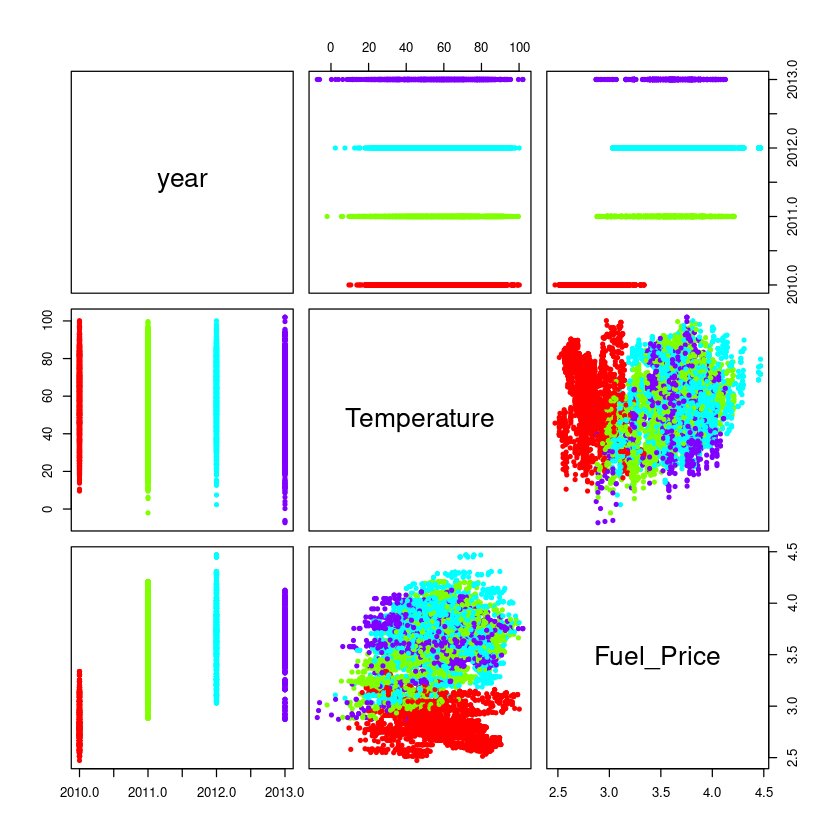

Fancy plots

Paint scatter plot by years.

pairs(data[, c(2, 5, 6)], pch =20, col =rainbow(4)[factor(data$year)])

Add density plot, correlation coefficient score, and confidence interval. (HINT: ??pairs.panels)

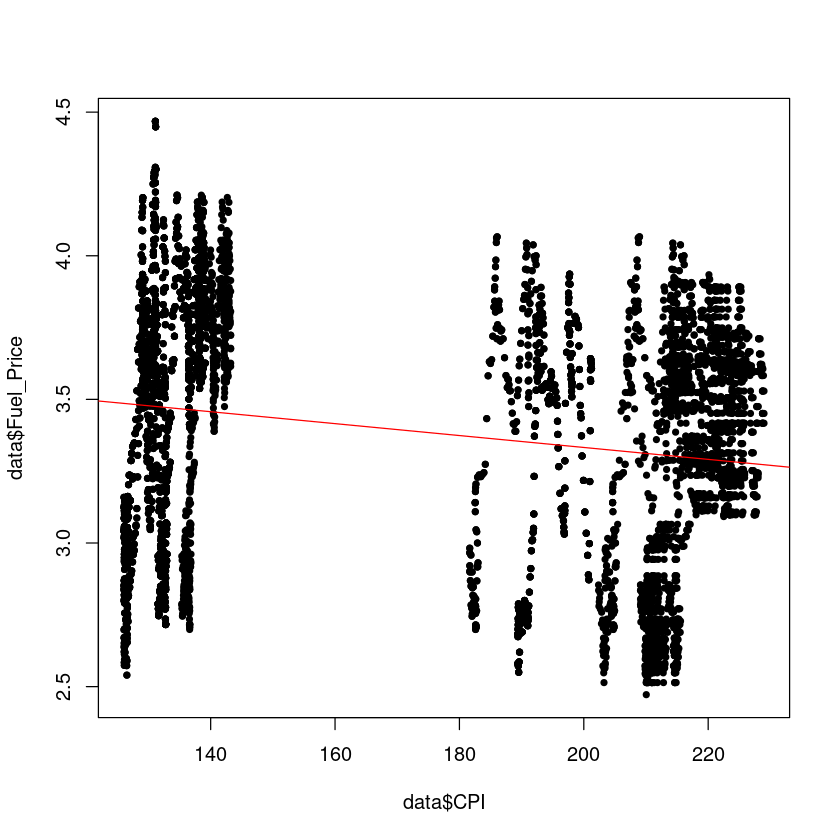

This section will try to fit a linear model with independent variables having a discrete data type.

Fit store, year, temperature, fuel price, and unemployment rate into the model. Note that store and year should be considered category data in this case.

This will return a long table. When we consider category information as a dependent variable, using a dummy variable is how we calculate.

What are the reference points for stores and years?

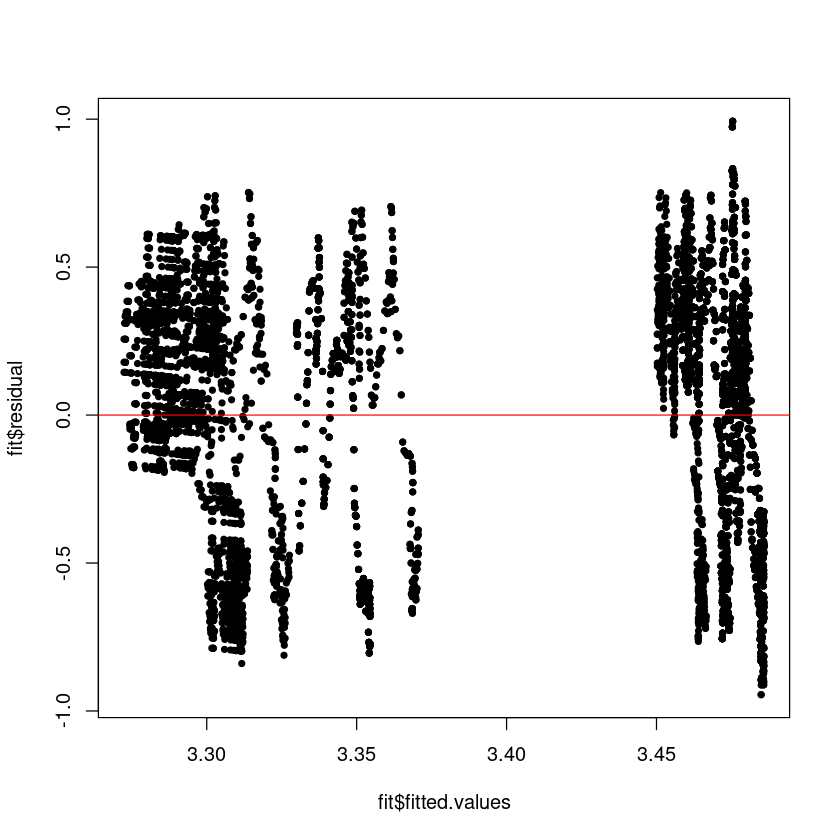

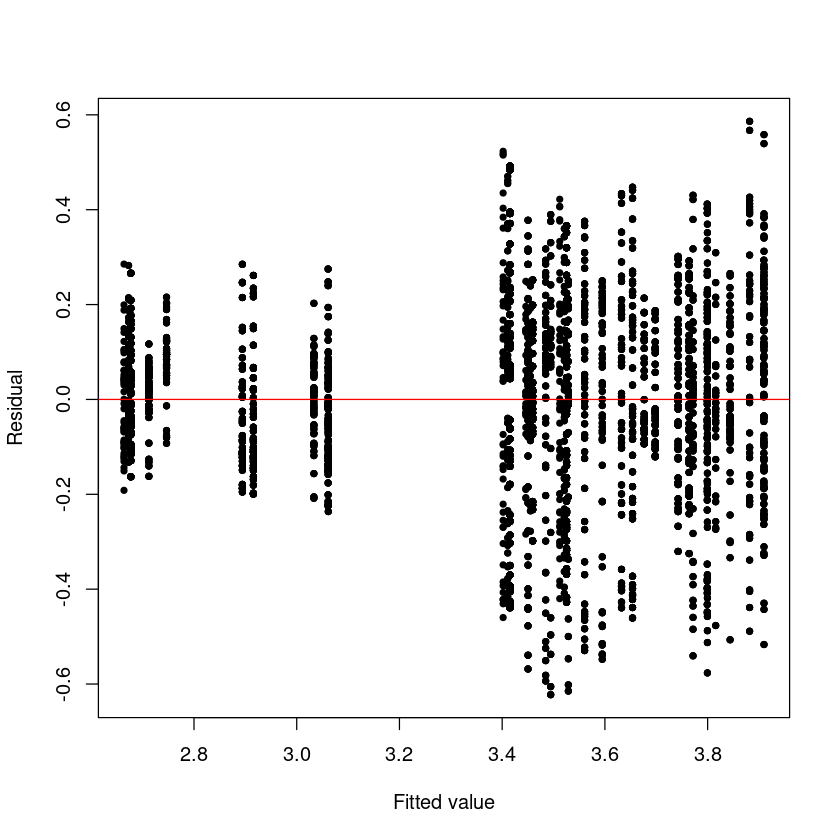

fit =lm(Fuel_Price ~factor(Store) +factor(year), data)summary(fit)

Fit a two-way ANOVA model: CPI = Store + year + e. - Do your degrees of freedom make sense? (If it is 1, you may forget to convert your data type as factor) - What conclusion can you make from this result?

fit =aov(Fuel_Price ~factor(Store) +factor(year), data)summary(fit)